In today’s globalized economy, individuals and businesses frequently earn income across national borders. While this creates opportunities for growth and expansion, it also introduces the challenge of double taxation. This occurs when the same income is taxed by two different countries, placing an extra financial burden on taxpayers. For professionals involved in international finance or cross-border services, understanding double taxation is essential for managing corporate audits and working effectively with international clients.

Why Double Taxation Occurs?

Double taxation Double taxation occurs when the same income is taxed either by one or more than one jurisdiction or taxing authority, either in the same form or in different forms. It generally takes two forms: direct and indirect.

Direct double taxation exists when two taxes are imposed on the same subject matter, purpose, by the same taxing authority, within the same jurisdiction, during the same taxing period, and the taxes are of the same kind or character . In the Philippines, this type of double taxation is generally not allowed.

On the other hand, indirect double taxation has the same elements except that the taxes are taxed by different taxing authorities. This form is typically allowed under Philippine tax rules.

Essentially, double taxation reflects a jurisdictional “conflict” over which authority has the primary right to tax an income. To resolve this, most countries apply a combination of principles to determine taxing rights.

- Residence Principle: A country taxes its residents on their worldwide income, regardless of where it is earned.

- Citizenship Principle: A country taxes its citizens on their worldwide income, regardless where they live or where the income is earned.

- Source Principle: A country taxes income earned within its territory, regardless of the taxpayer’s residency.

Example

When a resident of Country A earns income in Country B, both nations may claim the right to tax that income—Country A because the individual lives there, and Country B because the work occurred within its borders. Without intervention, taxpayers could lose a significant portion of their earnings to taxes in both countries.

So, if you live in one country but earn income in another, both countries may ask you to pay taxes on that same income—one because you’re a resident, and the other because the income came from their territory.

In simple terms, it’s like being asked to pay tax twice on the same earnings just because two countries both claim a right to it.

How DTAs Work

Double Taxation Agreements (DTAs) prevent or reduce double taxation through three main methods:

- Exemption Method – Income is taxed only in one country.

- Tax Credit Method – Taxes paid abroad are credited against domestic tax liability.

- Reduced tax rate method – allows both countries to tax the same income, but the source country agrees to apply a lower treaty rate instead of its normal domestic tax rate. It is commonly used for passive income such as dividends, interest, royalties, and rent in some occasions.

These mechanisms help eliminate or reduce the financial burden of being taxed twice on the same income.

Double Taxation Agreement in the Philippines

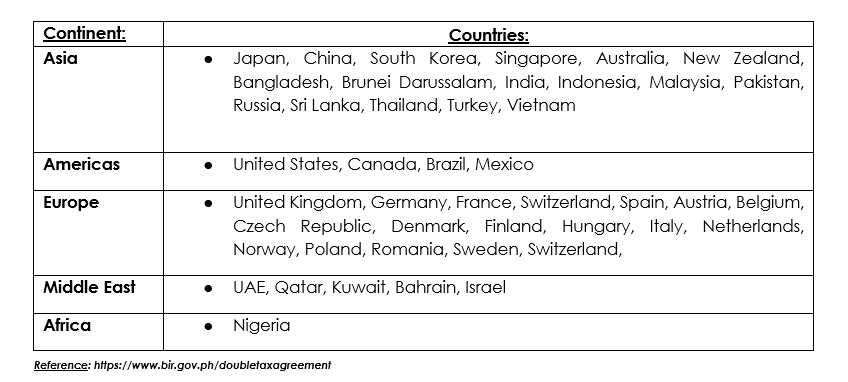

Currently, the Philippines has a network of 44 active DTAs with various countries. These treaties provide clear rules on which country has the primary right to tax different types of income, such as dividends, interest, royalties, and business profits. They often also set reduced rates to prevent excessive taxation and promote fair trade.

Key Takeaway

Double Taxation Agreements are essential for keeping the Philippine tax system fair and predictable, preventing the same income from being taxed twice across borders. Tools like the Tax Treaty Relief Application (TTRA) and Request for Confirmation (RFC) make it easier for taxpayers to claim treaty benefits and certify residency, reducing fiscal burden and fostering confidence in cross-border transactions.

By streamlining compliance and protecting taxpayers, DTAs, together with the TTRA and RFC, not only drive economic growth but also enhance the Philippines’ global competitiveness.

As international trade and investments expand, the question remains: how can we further sharpen these tools to unlock even greater opportunities for businesses and the economy?

Found this helpful? ♻️ Share and follow Babylon2K & UHY M.L. Aguirre & Co., CPAs for more.

P.S. Powered by hashtag#BethAI – ai.babylon2k.org, your intelligent assistant for tax, audit, accounting, and licensing.

Reference:

- Department of Finance, Republic of the Philippines. (2024, May 3). DOF leads conclusion of PH Cambodia DTA to protect Filipinos’ taxing rights and increase trade and investment across economic borders. https://www.dof.gov.ph/dof-leads-conclusion-of-ph-cambodia-double-taxation-agreement-to-protect-filipinos-taxing-rights-and-increase-trade-and-investment-across-economic-borders/?m

- Philippine News Agency. (2025, May 27). PH, Hong Kong start negotiations for Double Taxation Agreement. https://www.pna.gov.ph/articles/1250872?m

- PwC Philippines. (2025, December 19). Philippines – Foreign tax relief and tax treaties. PwC. https://taxsummaries.pwc.com/philippines/individual/foreign-tax-relief-and-tax-treaties?m

- Bureau of Internal Revenue. (n.d.). Philippine Double Taxation Agreements (DTA). Bureau of Internal Revenue. https://www.bir.gov.ph/doubletaxagreement?m

Article written by: Kyle Clarence L. Williams, CPA, MICB, RCA, CAT