For many Filipinos working independently today, understanding taxes is as challenging as finding clients. From freelance designers and online sellers to consultants and professionals, a growing segment of the workforce now operates outside traditional employment. With that independence comes a responsibility many are still learning to navigate: choosing how to be taxed.

Under Philippine tax rules, particularly following the reforms introduced under the Tax Reform for Acceleration and Inclusion (TRAIN) Law (Republic Act No. 10963), taxpayers/individuals engaged in business, trade or profession are given a choice that can directly affect their income: opt for the 8% income tax, or remain under the graduated income tax system with a 3% percentage tax or 12% VAT. At first glance, it seems like a technical matter. In reality, it is a financial decision that can mean the difference between paying what is due and paying more than necessary.

Who Can Avail of Each Tax Regime

Before comparing which option is more beneficial, it is essential to determine whether the taxpayer is even qualified to choose between them.

The 8% income tax option is available only to self-employed individuals and professionals who are non-VAT registered and whose gross sales or receipts do not exceed the ₱3,000,000 VAT threshold for the taxable year. Once a taxpayer becomes VAT-registered, whether by exceeding the threshold or by voluntary registration, the 8% option is no longer available.

In contrast, the graduated income tax system applies as the default regime for all individual taxpayers, including those who do not qualify for or do not elect the 8% option. Non-VAT taxpayers under this system are likewise subject to percentage tax under Section 116 of the NIRC, generally at 3% of gross receipts.

For mixed-income earners, the 8% option may apply only to business income without the ₱250,000 exemption, as it is already applied to compensation income. The option is likewise limited to individual taxpayers and does not extend to corporations.

Ultimately, the question is not only which tax regime is better, but whether the option is legally available in the first place.

A Simple Choice With Real Consequences

The 8% income tax option was introduced under Section 24(A)(2)(b) of the National Internal Revenue Code (NIRC), as amended by the TRAIN Law, as a simplified alternative for self-employed individuals and professionals. Instead of dealing with multiple layers of taxation, eligible self-employed individuals may pay a flat 8% tax on gross receipts exceeding ₱250,000, replacing both income tax and percentage tax.

For many taxpayers, this was a welcome development. It removed layers of computation and reduced compliance burdens. But the simplicity is deliberate, as it comes at a cost. The law does not allow deductions under this option. The tax is computed on gross income(*1), regardless of how much it actually costs to earn that income.

The Alternative: More Work, More Control

On the other side is the traditional system anchored on Section 24(A)(2)(a) of the NIRC, which imposes graduated income tax rates ranging from 0% to 35% on net taxable income. Here, taxpayers are allowed to deduct ordinary and necessary business expenses under Section 34 of the NIRC, reducing the amount subject to tax.

This is complemented by the 3% percentage tax under Section 116, applicable to non-VAT taxpayers, subject to temporary relief measures under subsequent laws (such as CREATE, which reduced the rate to 1% for certain periods)(*2).

On paper, this system appears more complex. But that complexity serves a purpose. The graduated system allows you to align your tax with your actual business situation. If your expenses are high, your taxable income goes down. In other words, while the 8% option prioritizes ease, the graduated system allows for strategy.

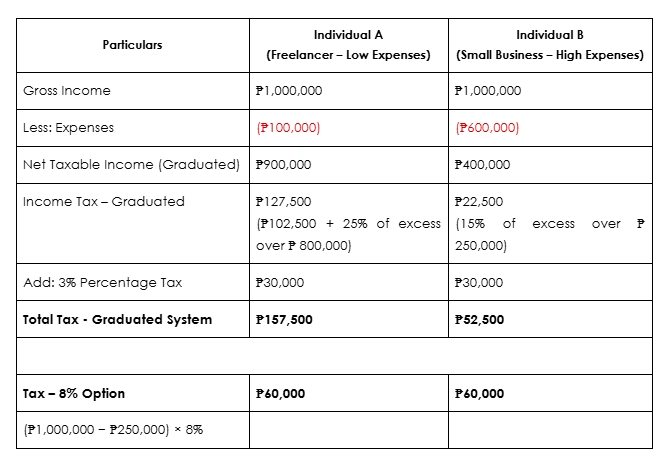

Where the Difference Becomes Real

Consider two individuals earning the same amount of ₱1,000,000 in a year, but with different cost structures.

For Individual A, the 8% option results in significantly lower tax.

But for Individual B, the graduated system becomes more favorable due to the ability to deduct substantial business expenses.

The effectiveness of a tax regime depends not on the rate, but on the structure of income and expenses.

The Common Misunderstanding

Despite this, many self-employed individuals default to the 8% option. Some assume it is always cheaper. Others choose it for convenience, without evaluating their financial position. Both approaches can be costly.

There’s a tendency to equate simplicity with savings, but that’s not always the case. Equally common is the belief that the graduated system is overly complicated or only suitable for larger businesses. While it does require proper documentation, it is not inherently impractical, especially when the potential savings are significant.

Most importantly, the choice of tax regime is not flexible within the year. It is generally exercised at the beginning of the taxable year and applies for the entire period, consistent with BIR guidelines.

A Matter of Awareness

What emerges from this discussion is not just a technical comparison, but a broader issue of tax awareness. Unlike employees, whose taxes are withheld automatically, self-employed individuals must actively manage their obligations. This includes not only filing returns, but also making informed decisions about how they are taxed.

In this context, the ability to choose between tax regimes is not merely an administrative feature, but a form of control. But control requires understanding. While the tax system offers flexibility, the choice is only as good as the understanding behind it.

The Bottom Line

For self-employed individuals, taxation is no longer a passive obligation. It is an active decision point. The choice between the 8% income tax and the graduated system is not about finding the easier option, but the more appropriate one.

Because in a system that allows choice, the real advantage belongs to those who understand it.

(*1) “Gross income” refers to the total earnings, receipts, or revenues derived from the conduct of trade or business or the practice of a profession, without any deduction for costs or expenses, in accordance with Section 32(A) of the National Internal Revenue Code of 1997, as amended.

(*2) The percentage tax rate was reduced from 3% to 1% under Republic Act No. 11534 (CREATE), as implemented by RR No. 21-2020 and RR No. 18-2021, covering the period from July 1, 2020 to June 30, 2023

Article written by: Paul Jericho Aguila