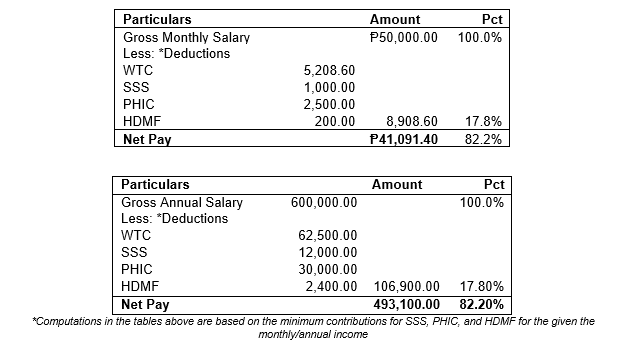

In the Philippines, the true measure of wealth lies not in gross income but in disposable income—the amount left after taxes and mandatory contributions. As one maxim reminds us, “A penny saved is worth two pennies earned, after taxes.” For compensation-income earners, statutory deductions such as withholding tax on compensation (WTC), Social Security System (SSS), PhilHealth, and Home Development Mutual Fund (HDMF) contributions can erode nearly one-fifth of their earnings.

Consider the case of an employee earning ₱50,000 monthly. After deductions, the net pay falls to ₱41,091.40, representing a 17.8% reduction. On an annual basis, this translates to approximately ₱106,900 in total deductions.

Why De Minimis Benefits Matter

Taxes remain the lifeblood of government, but the law provides mechanisms to ease the burden on employees. One such mechanism is the grant of de minimis benefits.

De minimis benefits are modest perks or allowances of relatively small value that employers provide to employees as part of the employment relationship. These benefits are designed to foster employee well-being, goodwill, and workplace efficiency. Under the Tax Code and applicable regulations, de minimis benefits are excluded from gross income and are therefore exempt from income tax, withholding tax on compensation, and fringe benefit tax.[1]

This means that even without raising an employee’s actual salary, employers can ease employee financial burden by restructuring payroll and allocating a portion of compensation to non-taxable benefits. The result is a win-win: employees enjoy higher take-home pay due to reduced taxes, while employers foster goodwill and support employee welfare without incurring additional costs.

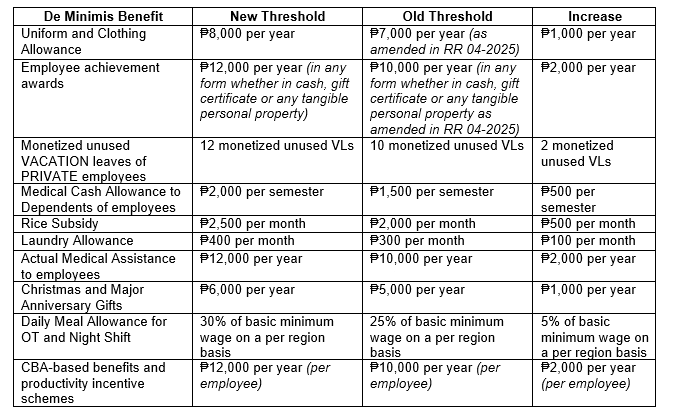

Recognizing the importance of de minimis benefits, the Bureau of Internal Revenue (BIR) issued Revenue Regulations (RR) No. 29-2025 on December 22, 2025, effective January 6, 2026. The regulation amended RR No. 2-98 by raising the non-taxable thresholds for several de minimis benefits.

Quantifying the Impact

The impact of these adjustments is significant. If employers maximize the allowable thresholds, an employee’s taxable compensation can be reduced by at least ₱17,624.75 annually.

For a company with 100 employees, this translates to an increase in collective take‑home pay of at least ₱1,762,475.00—achieved solely through strategic payroll structuring, without costing a single extra peso. Employees benefit from higher disposable income, while employers enhance employee morale and loyalty without incurring extra tax liabilities. Talk about wise and thoughtful tax planning!

Conclusion

On a final note, RR No. 29-2025 shows that enhancing employee welfare does not always require higher wages—though such increases are certainly welcome. By restructuring compensation and making full use of de minimis benefits, employers can reduce the tax burden on employees while strengthening morale and productivity. In a time when every peso matters, aligning payroll practices with updated tax regulations becomes both a practical financial strategy and a thoughtful way of supporting the workforce.

[1] Section 32(B)(7)(e) of the National Internal Revenue Code (NIRC), as amended.

Article Written by: Imy Eulin, CPA