Revenue Regulations (RR) No. 9-2025, issued on February 27, 2025, implements Section 295(D) or the VAT provisions of Republic Act No. 12066 (CREATE MORE Act) concerning the tax treatment of local sales of goods and/or services by Registered Business Enterprises (RBEs). Under this regulation, all local sales by RBEs are subject to 12% VAT, regardless of their income tax regime or location (including sales within freeports or economic zones), unless otherwise exempt or zero-rated under the Tax Code.

Importantly, for business-to-business (B2B) transactions, the liability to pay and remit VAT is shifted to the buyer, while the RBE-seller must invoice the sale showing “VAT on Local Sales” separately. For business-to-consumer (B2C) transactions where the buyer is not engaged in business, the seller remains responsible for remitting the VAT collected. The regulation also outlines procedures for invoicing, filing, payment, and VAT certification for local sales, and provides optional VAT registration for certain RBEs under special tax regimes.

On December 10, 2025, RR 1-2026 was issued by the BIR to provide guidance on how RBEs can better comply with the treatment of VAT for their Local Sales of Goods and/or Services. Let’s take a deeper look at the salient provisions of the said revenue regulations.

The Amendments

VAT on B2B Local Sales by RBEs

As a general rule, VAT on purchases of goods from economic zones or freeports must be paid on a per-transaction basis using BIR Form 0605, with payment to be made prior to the release of goods from the economic zone or freeport.

However, in the case of bulk purchases covered by multiple invoices, the buyer has the option to consolidate the VAT payment into a single transaction, remitting the amount using BIR Form 0605.

Optional VAT Registration

RBEs who enjoy 5% Special Corporate Income Tax (SCIT) or Gross Income Earned (GIE) regime may opt to register as a VAT taxpayer for the purposes of their local sales. Such registration shall not affect the RBE’s entitlement to existing fiscal and non-fiscal incentives, including any VAT-related incentives.

Exclusions from Coverage of VAT on Local Sales under Section 259(D) of the Tax Code, as amended

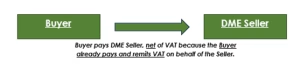

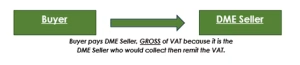

VAT-registered Domestic Market Enterprises (DMEs) that do not qualify for VAT-zero rating on local purchases or VAT exemption, despite being registered with any Investment Promotion Agencies (IPAs), are generally subject to VAT on all their purchases, unless explicitly exempted under other provisions of the Tax Code. This includes entities registered with the Board of Investments (BOI) that are not benefiting from incentives under Title XIII of the Tax Code, as amended. It is important to note that in a Business-to-Business (B2B) transaction between a buyer and a DME-Seller, the VAT is generally withheld by the buyer. However, the issuance of RR 1-2026 clarifies that the DME-Seller now collects and remits the VAT, thereby allowing DMEs to offset their input VAT against their Output VAT. As a result, this makes VAT refund less of an option at this point. To further illustrate:

Before RR 1-2026 (per RR 9-2025):

After RR 1-2026:

Furthermore, in the aforementioned transactions, the status quo applies where the respective seller will be liable for VAT.

Extension of Invoice Reconfiguration

The deadline for reconfiguring Registered Business Enterprises (RBEs) that use registered Cash Register Machines/Point-of-Sales (CRM/POS), Computerized Accounting Systems (CAS), Computerized Books of Accounts, and other registered invoicing systems has been extended to December 31, 2026. This reconfiguration involves updating the term “VAT/VAT Amount” to “VAT on Local Sales” in these systems.

Key Takeaway

Revenue Regulations No. 1-2026 represents a significant step toward strengthening the VAT compliance framework for Registered Business Enterprises (RBEs). By introducing clearer rules and reinforcing transparency in VAT reporting, the regulation aims to minimize errors, curb potential tax leakage, and create a more structured compliance system. Yet, beyond the mechanics of compliance, the greater challenge—and opportunity—lies in how RBEs respond to these changes.

Rather than viewing the regulation merely as an additional regulatory burden, RBEs may consider it an opportunity to reassess their internal processes, strengthen their tax governance, and build greater trust with tax authorities and business partners. The shift also raises practical questions: How should RBEs manage previously accumulated input VAT now that DME-sellers themselves are responsible for remitting VAT on B2B transactions? And more importantly, how can businesses transform compliance obligations into operational efficiencies and stronger financial transparency?

Ultimately, the future of tax compliance is not simply about meeting regulatory requirements—it is about using those requirements as a catalyst for better systems, stronger accountability, and a culture of integrity within the business ecosystem.

As the regulatory landscape evolves, the question remains: will businesses merely comply, or will they adapt strategically and lead the way in shaping a more transparent and efficient tax environment?

Found this helpful? ♻️ Share and follow Babylon2K & UHY M.L. Aguirre & Co., CPAs for more.

P.S. Powered by #BethAI – ai.babylon2k.org, your intelligent assistant for tax, audit, accounting, and licensing.

Article written by: Kyle Clarence L. Williams, CPA, MICB, RCA, CAT