In Bureau of Internal Revenue (BIR) tax audits, some of the most expensive findings do not begin with fraud or aggressive tax planning. They begin with something quieter — a missing withholding tax on an otherwise legitimate expense. A company pays a consultant, records the cost, and deducts it in good faith. Months or years later, during an audit by the BIR, that same expense is disallowed, not because the service was fictitious, but because the required Expanded Withholding Tax (EWT) was never withheld and remitted.

What looked like a minor compliance lapse can escalate into layered tax exposure: deficiency income tax, a 25% surcharge, 12% annual interest, compromise penalties, and a separate liability for the unremitted withholding tax itself. In the Philippine system, withholding tax is not just a collection mechanism, it is an enforcement tool and, in many cases, the gatekeeper to whether an expense is even allowed as a deduction.

The Legal Anchor: Why Expenses Get Disallowed

Under Philippine tax rules, certain expenses are deductible only if the taxpayer complies with the withholding tax requirement attached to that payment. This is what tax practitioners refer to as a “condition precedent to deductibility.”

For taxable periods up to 2023, failure to withhold EWT could trigger a permanent disallowance of the expense during a BIR audit.

Here’s how that plays out during an audit:

- The BIR reviews expense accounts — professional fees, rentals, commissions, contractor payments.

- The examiner checks whether the company filed the proper EWT returns (typically BIR Form 1601-EQ) and included the payees in the alphalist.

- If no withholding was made when it should have been, the expense is flagged.

From there, the financial domino effect begins:

- Liability for the unwithheld EWT

- 25% surcharge on the deficiency tax

- 12% annual interest (computed from the original due date until payment)

- Compromise penalties

So a ₱1,000,000 professional fee paid without withholding does not just result in a small penalty. It can trigger layered assessments that far exceed what the company expected when it first recorded the expense.

From 2024 onwards, under the current EOPT guidance, the treatment has changed: the BIR now generally requires payment of the deficiency EWT along with applicable surcharge and interest, but the related expense remains deductible once the withholding tax is properly remitted.

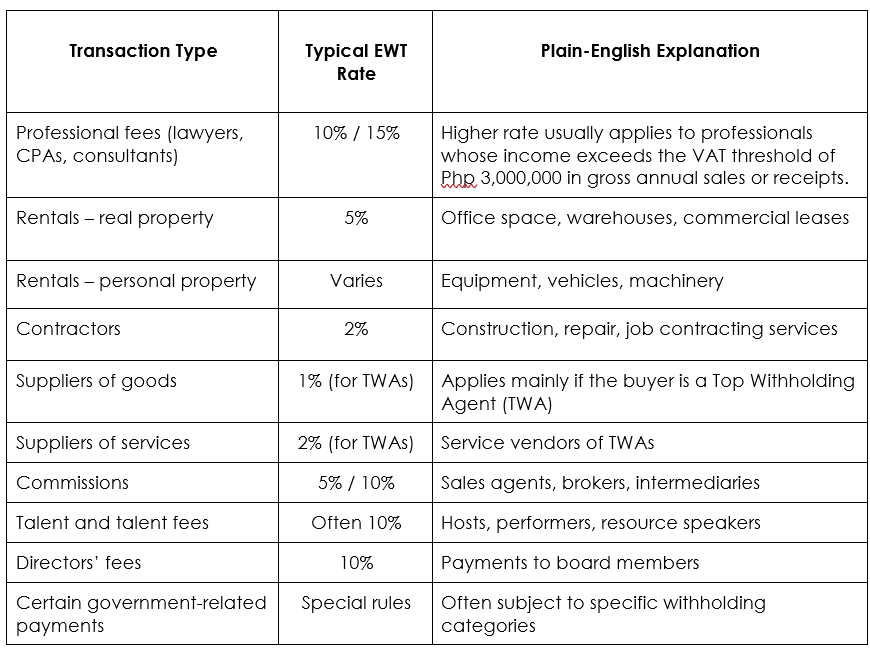

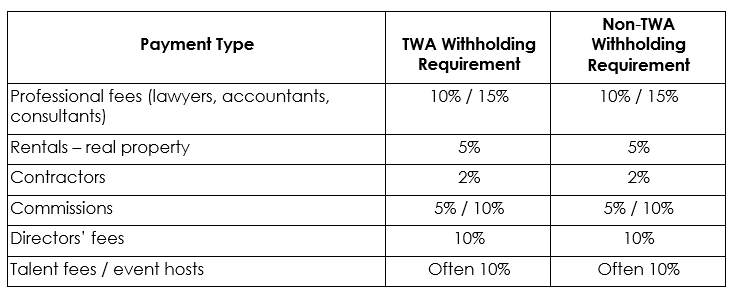

Common Transactions Subject to EWT

One reason this issue is widespread is that many everyday business payments fall under EWT rules. Below is a simplified view of commonly encountered categories:

What surprises many business owners is that these are not exotic transactions. They are routine operating expenses.

Top Withholding Agents vs. Everyone Else

A major source of confusion is the distinction between Top Withholding Agents (TWAs) and non-TWAs. A TWA is not just “a large taxpayer” in the informal sense. Under the BIR’s current criteria, a taxpayer becomes a TWA when it meets certain objective financial thresholds based on gross sales/receipts or gross purchases in the preceding taxable year. These thresholds depend on the taxpayer’s Revenue District Office (RDO) classification:

- For taxpayers registered under Groups A and B, the minimum is ₱12,000,000 in gross sales/receipts or gross purchases in the preceding year.

- For taxpayers under Groups C, D, and E, the threshold is ₱5,000,000 in gross sales/receipts or gross purchases in the preceding year.

Once a taxpayer meets the applicable threshold and is officially published or notified by the BIR as a TWA, the withholding obligations on purchases take effect from the first day of the month following publication or notice. Once classified, a TWA is required to withhold:

- 1% on purchases of goods

- 2% on purchases of services

This is on top of other withholding categories that may already apply.

Non-TWAs are generally not required to withhold the 1%/2% on ordinary purchases of goods and services. However, they must still withhold on items like professional fees, rent, commissions, and contractors.

The compliance risk emerges when companies either:

- Fail to realize they have been classified as a TWA, or

- Assume that being a non-TWA means they have no withholding responsibilities at all.

Both assumptions routinely surface in audits and can lead to expense disallowances. To clarify, here is a brief comparison of withholding requirements for common payments:

Note: The main difference is that TWAs must withhold 1% on goods and 2% on service purchases, which does not apply to non‑TWAs. Other withholding obligations, such as professional fees or rentals, apply to both.

Frequently Missed Withholding Areas

During Letter of Authority (LOA) examinations, BIR auditors often focus on specific expense lines known to carry withholding risks:

- Professional fees paid to individuals without any tax withheld

- One-time consultants engaged without formal onboarding

- Rent paid to individual lessors who issue handwritten receipts

- Talent fees for events, hosts, speakers

- Sales commissions paid informally or via reimbursements

- Directors’ fees booked under “representation” or “honorarium”

- Retainers labeled as reimbursements but actually covering professional services

- Payments net of VAT but with no EWT withheld

- Service contracts misclassified as purchase of goods

These are attractive audit targets because they are high-value, recurring, and often supported by documentation that proves the expense occurred, but not that withholding was done.

Transactions Generally Not Subject to EWT

Not every payment requires withholding, but exemptions must be defensible and documented. Examples often discussed include:

- Certain casual or non-regular suppliers, though frequency and nature of transaction matter. Under the BIR’s EWT rules, a “regular supplier” is one with whom the buyer has transacted at least six (6) times, regardless of the transaction amount, either in the current year or the preceding year.

- Credit card purchases, where withholding obligations may shift to the merchant acquiring bank under specific rules

- True reimbursements, where the employee or officer advanced money and is merely being repaid — not earning income

- Payments to entities with valid BIR exemption certificates

- VAT itself, which is generally not subject to EWT (except in specific withholding VAT systems)

- Certain transactions with government entities, depending on applicable regulations

The key audit principle is simple. If you claim an exemption, you must be able to show the paper trail.

Other Overlooked Risk Areas

Beyond individual transactions, systemic gaps often worsen exposure:

- No reconciliation between Form 1601-EQ and expense accounts in the AFS

- Mismatch between Alphalist of Payees and the general ledger

- Late remittances, triggering interest even if tax was eventually withheld

- Incorrect application of 10% vs. 15% on professional fees

- Payments to non-residents without considering tax treaty implications

- Confusion between gross vs. net basis in computing withholding

- Failure to obtain supplier TINs and registration details

Each of these may seem minor in isolation. Together, they create a pattern auditors interpret as weak withholding controls.

Withholding Tax as a Governance Signal

Why does the BIR focus so heavily on EWT? Because withholding tax creates traceability and functions as an advance tax payment. It links the payer and the payee in the tax system, allowing businesses to remit a portion of their tax liability to the government as transactions occur. This benefits both sides: the government ensures timely collection, while taxpayers spread their tax obligations over the year, lessening the cash flow burden. When a company withholds and remits properly, it signals structured compliance; when it does not, it raises the question: what else might be unreported?

From a governance standpoint, withholding compliance is a proxy for internal control discipline. It shows whether finance teams understand tax rules, monitor vendor classifications, and align accounting with regulatory obligations. For the Management, this turns EWT from a back-office task into a risk management priority.

More Than a Clerical Detail

Withholding tax in the Philippines is far more than an early collection mechanism; it serves as a tool for enforceable traceability and an advance payment of tax, benefiting both the government and the taxpayer. Proper withholding signals structured compliance, ensures staggered remittance, and links the payer and the payee in the tax system.

Under the previous EOPT rules (2023 and prior), failure to withhold could also lead to the disallowance of the related expense for income tax purposes, turning even legitimate payments into layered assessments. Today, however, the disallowed expense due to non-withholding is no longer assessed, and only the unremitted EWT with applicable penalties and interest remains as a liability.

Businesses that treat EWT as a clerical afterthought still risk audit scrutiny, because withholding underpins both expense recognition (for prior periods) and governance signals. In Philippine taxation, the simple act of withholding—or failing to do so—can determine whether an expense survives scrutiny, while also managing cash flow through advance tax payment, shaping both regulatory credibility and financial planning.